Due to confidentiality, images and data are limited to what could be made available publicly

Introduction

As part of Lloyds Banking Group’s digital transformation initiative, the Commercial Lending division sought to increase adoption of its online Asset Finance journey. Despite substantial investment in digital infrastructure, only a small percentage (in the single digits) came through the digital channel, compared with the traditional telephony and field channels.

I led the research project aimed at uncovering the reasons behind this low adoption rate, identifying actionable ways to shift customer behaviour toward digital, and overseeing the implementation of the proposed solutions.

The challenge

Research question:

Why does the digital Asset Finance journey represent only a fraction of total sales?

The business wanted to understand how commercial customers engaged with Asset Finance, their pain points, and what would motivate them to use the digital platform instead of relying on phone or in-person channels.

Team and my role

Our project team included:

- Product Owner

- UX Designer

- Business Analyst

- System Architect and Engineers

- Customer Journey Managers

I was the sole researcher dedicated to Asset Finance, responsible for end-to-end research activities — from planning and fieldwork to analysis and stakeholder communication. I also mentored new Customer Journey Managers on how to build journey maps and conduct user-centred research.

Research Approach

We adopted a mixed-methods approach, integrating qualitative and quantitative research across the discovery and delivery phases.

1. Desk Research

I began by benchmarking our competitors, from NatWest’s Lombard (market leader) to niche finance providers, mapping their customer journeys and identifying best practices. I also performed a heuristic evaluation of Lloyds’ own digital journey, uncovering friction points and missing features.

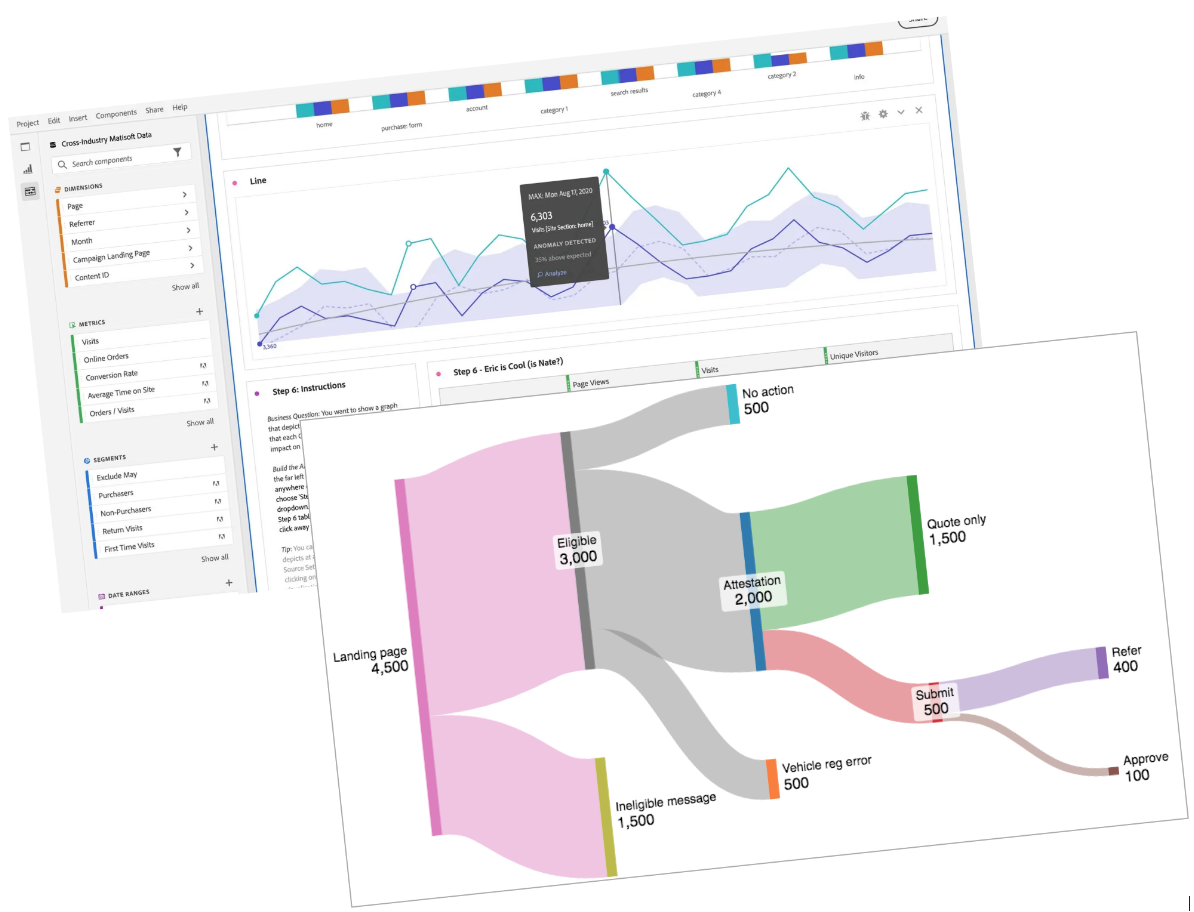

2. Site Usage Analysis

Using Adobe Analytics and management information logs, I tracked how customers navigated our site. A custom Sankey diagram visualised where users dropped out, exposing “dead ends” and moments of confusion. These insights directly informed redesign priorities.

3. Customer Interviews and Usability Testing

Through one-hour semi-structured interviews with recent Asset Finance customers, we explored:

- How they decided to take out finance

- How they chose a provider

- Their perceptions of the digital vs. telephony journey

- We also tested prototypes designed in Figma to validate usability and desirability.

4. Colleague Shadowing

To understand the success of non-digital channels, I spent two days shadowing and interviewing the telephony team in Southampton. Their ability to provide real-time advice and reassurance explained why many customers preferred phone support over online self-service.

5. Surveys (NPS and Exit)

Using Qualtrics, I collaborated with the Customer Insights team to analyse open-ended feedback from post-service and exit surveys — moving beyond word clouds to perform a full thematic analysis of pain points and expectations.

6. Customer journey map and stakeholder workshop

I created a customer journey map to engage stakeholders, bringing a holistic view including user needs or jobs to be done (what happen before they visit our digital journeys) and also the outcomes that bring business value (after they click Submit).

Key Findings

- Human reassurance matters.

Customers valued the guidance and expertise of telephony staff, especially for complex purchases. Also, experienced colleagues were very good at knowing the needs of repeat customer. - The digital journey was fragmented.

With multiple redundant steps and unclear eligibility checks, the online process felt cumbersome. - Data continuity was missing.

Customers wanted features that mimicked the telephony experience — such as saving quotes, uploading documents, and tracking progress. - Behavioural inertia.

Many customers had long-standing habits of calling their relationship manager, viewing digital as riskier or less personal.

Recommendations

- Design for customer outcomes, not system constraints.

Focus on solving real user problems rather than aligning solely with internal processes. - Bring the best of human service online.

Features like a customer dashboard, quote saving, and progress tracking could bridge the gap between human and digital. - Simplify and streamline.

Eliminate dead ends and redundant steps, such as overcomplicated eligibility or asset checks.

Outcomes and Impact

Despite resource constraints that put some larger features on hold (like the dashboard), the implemented optimisations led to tangible results:

- Doubled the number of digital submissions

- Improved user experience through clearer pathways and reduced dropouts

- Increased leadership engagement in customer-centric design methods

Reflection

This project highlighted the power of holistic, mixed-methods research in revealing not just what customers do, but why they behave that way. It also demonstrated the value of communicating insights visually and collaboratively — through journey maps, Sankey diagrams, and stakeholder workshops.

By combining empathy, data, and design thinking, we took a major step toward building a more customer-centric digital journey for Lloyds’ business clients.